Below, you’ll find the Reasoning & Rationale to what we call a Bill-Request. Once certain milestones are met, as defined HERE, lawyers will be called upon to draft what will then become a Bill-Demand to Congress and the President.

What you’re voting for, in perspective:

When President Harry Truman left the White House in 1953, he knew he and his wife, Bess, would experience a financial sea-change in their lives — for he had no pension, despite having served two terms, in no less than the highest office in the land. His only source of federal income: a pension from the Army of 112 dollars and 56 cents a month. Financially constrained, Harry and Bess moved back into their old house in Independence, Missouri. This despite numerous lucrative job offers — among them: one for $100,000 and another for $1 million a year. (That’s about $1 million to $10 million in modern-day dollars, for what it could buy back then.) “I could never lend myself to any transaction, however respectable, that would commercialize on the prestige and dignity of the office of the presidency,” he wrote.

Moreover, Truman refused to endorse commercial products for money, or consult for fees. He refused to lobby. He declined all overtures to peddle influence, for any amount of compensation.

According to the book Harry Truman’s Excellent Adventure: in Independence, Missouri, Truman would ask that folks not call him Mr. President. He’d take morning walks through the town square. He’d reply to mail from ordinary Americans. He’d talk to random walk-in’s who visited the humble office he kept. Said Truman: “Many people feel that a president or an ex-president is partly theirs … and that they have a right to call upon him.” In accordance, Truman listed his telephone number in the directory.

Washington D.C. may not miss you anymore, Mr. Truman. But we do.

In voting for this bill-request, you (as a voter) are saying “I admire what Harry Truman did after he retired from public service. He was a Democrat that both Republicans and Democrats should look up to, as shining example of what it means to serve. Too bad that private life — after modern-day public $$$ervice — has now devolved into abominations like post-presidential speeches for up to $750,000 a pop and post-presidential decadences like vacations aboard 300-million-dollar 454-foot super-yachts of billionaires.”

The following was first published in 2012, and updated in 2017.

Ladies and Gentlemen, prepare yourself now for a front-row seat to the spectacle of our Nobles and Rulers striking it rich in Money City — i.e. Washington DC — where, at one of the city’s new hotels, a vodka martini can go for near 4 times the federal minimum wage — $30 including tax and tip if you’re a mid-level mover-and-shaker, and $23.27 (not including tip) for anyone else there, trying to take in how far our nation’s capital had come, from a meaningful place of Public Service to a bottomless pit of public $$$ervice.

Where to begin when it comes to corruption in our capital, is like a maze, in that it dazes and confuses any honest onlooker trying to make head or tail of it. But — just for the heck of it — let’s start with these tidbits or appetizers of corruption in action, because the main meal or entrée is a whole lot harder to swallow:

(1) Wall Street’s banks implicated in frauds, such as foreclosure fraud (or foreclosing on people the banks didn’t have a right to, because the banks had phony’d up the paperwork to throw homeowners out of their homes) have settled with the government with settlement dollars that were later allowed to be tax-deductible for the most part.

(2) In Dec 09, the government granted Citigroup permission to repay taxpayers $20 billion in bailout money. Despite Citi being still in tatters, financially, the idea was: The bailouts had put restrictions on executive compensation, yet the execs wanted to be compensated the way they dreamed of being compensated, and returning $20 billion to the taxpayer was one way to get executive compensation flowing like it used to flow, pre-bailout. So Citi gave Treasury the $20 billion and, in return, Treasury gave Citi $38 billion back in tax breaks.

(3) Pretty much every working American, no matter their financial well-being or struggle, experienced a tax increase starting 2013 with the payroll tax hike, equal to about a thousand bucks more taken away from a household earning a median income of about $52,000 a year. (The fact that this tax break, for mostly the poor and the middle class, was allowed to lapse only after President Obama’s re-election, was no accident by the Democrats.) Despite a $125 billion payroll tax hike hitting up everyone in the middle class and poor — yes, that includes those of you on a minimum hourly wage, as well — it’s important you know that there were $60-some billion in tax breaks for the usual suspects in 2013 alone, including:

- (i) breaks for offshore loans (hooray for banks);

- (ii) breaks for Liberty Zone bonds that helped bankroll luxury high-rises in lower Manhattan, including Goldman Sachs’ spanking new 200 West Street global headquarters;

- (iii) breaks for the politicians’ perennial buddies: the hedge fund and private equity bigwigs, who’ll get to make a hundred million bucks or a billion bucks in a year at a discounted tax rate, while all the suckers they see around them, making little money, pay almost twice that, because those itsy-bitsy teeny-weeny people, making small dough, can’t buy the politician the way the big-dough-makers can.

(4) In the aftermath of the financial crisis of 2008, the U.S. Treasury changed the tax code to favor and encourage bank mergers, figuring perhaps that the only way to taxpayer-protect and bail-out Wall Street at their next self-concocted crisis was to make the already Too Big To Fail banks even bigger. Consider, for example, the changes made in 2008 to Section 382 of the U.S. Tax Code…

(FYI: Congress designed Section 382 in 1986 to counter corporate abuse of the tax code by strictly restricting the practice of profitable corporations buying up shell companies that were harboring losses, so that the profits at the parent could be offset by those losses.)

…On Sep 30 2008, the Treasury unilaterally amended Section 382 to give banks the benefit of the tax-dodge, a windfall worth up to an estimated $140 billion to the banks.

Within days of that move, former Treasury officials, working for the banks on the other side of the revolving door, met with Assistant Secretary of the Treasury for Tax Policy, Eric Solomon, to ask that even foreign banks be allowed to get in on the dodge.

Per the demand of the U.S. Constitution, did Treasury ask (and hope) that Congress make the change? No — Treasury made the alteration on its own, leaving many to question its legality. “Did the Treasury Department have the authority to do this? I think almost every tax expert would agree that the answer is no,” said George K. Yin, the former chief of staff of the Joint Committee on Taxation. “They basically repealed a 22-year-old law that Congress passed, as a backdoor way of providing aid to banks.”

But what did Members of Congress do about Treasury’s invasion into their Constitutional territory? Yep, you guessed it: Nothing! Why mess with Public $$$ervice. Matter of fact, the staff of Senator Max Baucus (D-Montana), chairman of the Finance Committee, reportedly asked that an entire conference call about the modification to Section 382 be kept secret from the public.

(5) In Jan 2018, we learned that the Federal Reserve had paid Wall Street banks, both foreign and domestic, $25.9 billion in interest on excess reserves, $3.4 billion in interest on securities subject to repurchase, and $784 in dividends for owning the 12 Regional Banks of the Federal Reserve in Atlanta, Boston, Chicago, Cleveland, Dallas, Kansas City, Minneapolis, New York, Philadelphia, Richmond, St. Louis, and San Francisco. (Yes, Wall Street overtly owns these institutions of the taxpayer, while other institutions — like our Treasury and financial regulatory authorities — are ‘owned’ covertly). In grand total, we’re taking about over $30 billion in payments by the Fed here, in what financial commentator Wolf Richter rightly called “the easiest, most risk-free, sit-on-your-ass profit that banks ever made in the history of mankind.” By the way, the magnanimous interest on excess reserves (IOER), totaling $25.9 billion in 2017 alone, was a mega-gift to the banks that began Oct 3 2008, under Section 128 of the Emergency Economic Stabilization Act (aka Bank Bailout Act) of 2008, authorizing the Federal Reserve to begin paying such interest, with no end in sight going forward into 2018 and beyond.

For each of the six years starting 2008 ending 2013, the Gallup polling organization found Americans quoting the American economy as the #1 problem in the nation. However, in 2014 and 2015, Americans found the American government to be the #1 problem in the country. Not accidentally, Americans’ identification with both the Republican and Democratic parties, descended to all-time historic lows in 2016, per Gallup — a steepening trend-line predicted long ago for the decay and demise of both parties by Nov 3 2020.

Increasingly large majorities of Americans insist America’s on the wrong track, but if you were looking for what’s wrong specifically, then look no further than at the thickest bills with the sweetest names.

There was a time when ‘complex’ bills, like the Banking Act of 1933, used to be short — a few dozen pages at most. Now, when there’s nothing to hide, the bill is still short. When there’s something to hide, the bill is long. The more there is to hide, the longer it gets. When there’s everything to hide, count on a bill long enough to make Tolstoy’s 1225-page novel, War & Peace, seem like a short story for toddlers.

If you have even an inkling of doubt about that, look no further than Public Law 111–203, the so-called “Wall Street Reform and Consumer Protection Act” that effectively institutionalized backdoor bailouts of systemic banks via the Treasury and the Fed. 848 pages long to begin in 2010, Public Law 111–203 was by July 2013 (when we last peered at it) nearly 14,000 pages longer and only 40% complete in its rule-writing phase. (This being the phase when the Wall & K Street lawyers & lobbyists begin to carve out exceptions, exemptions, and loopholes for their own benefit.) 14,000 pages longer by July 2013, means we may very well end up with a final document that’ll be 35,000 pages long, years from then.

So who’s writing the rules of Wall Street Reform? In theory, regulators. In practice, though, they’re being ghostwritten by the banks and their fleet of lawyers/lobbyists seen crawling the hallways of Capitol Hill from time to time… no, scratch that, ALL THE TIME.

In July 2013, the Sunlight Foundation would reveal: “In the 152 weeks our data cover, we find 59 weeks in which regulators met with financial sector representatives at least once every single day, and 47 weeks in which they met with financial sector representatives at least four times.”

As a result, predictably, Wall Street Reform, signed into law by President Obama to much pomp, splendor, and fanfare, as an end to bailouts happening ever again, DID NOT END BAILOUTS! Matter of fact, 111-203 enshrined bailouts at the next crisis, circa 2019 … and if you doubt us about that, read HERE and HERE and we will most assuredly erase that doubt.

Yes, a bill’s not done after our politicians are done voting for it — hardly — especially if the bill is designed to reign in Wall and K Street. The politicians vote for the shell of the bill, then Wall and K Street take over to fill the shell with their own stuffing.

About how bloated legislation had become in modern times, we wrote:

If the People actually found out what was in some of these gargantuan bills, their blood would boil. If voters found out what was in some of these monstrosities, it would’ve sent near every established member of Congress, especially the senior-most bunch, packing at their next election to the inflexible confines of perpetual political oblivion. Would’ve sent some Presidents packing too.

Why? Because a patient perusal of those bills, will make every one of them reek of corruption on some page or the other, and smell of a sellout on another.

So, no wonder our legislators like their legislation to be thousands upon thousands of pages long and written in incomprehensible legalese, instead of 10 or 20 or 30 pages long and written in comprehensible English. It is, after all, easy to hide something bad — something detrimental to the public interest — in a 10,000 or 20,000 or 30,000 page legal leviathan, when there’s ample space to bury it, deep inside.

In Congress, July 4 1776, the unanimous Declaration of the thirteen United States of America was just about a page or so long. Super-sized bills are the subterfuge of choice of parasites. Something as vast and all-encompassing as the US Constitution, and all its 27 Amendments, encompass just 31 standard pages. Notice the absence of parasites in it.

By late 2016 and heading into the election of Nov the 8th, corruption had over-crowded and over-run the hallways of political power in DC to such a degree, that a large part of the nation’s electorate had begun to recognize it as an existential threat to their everyday lives. Matter of fact, by late 2016, that cognition had found its way into a place of primary residence in the America psyche, so much so that corruption ranked as follows in the widely reported Chapman University Survey on American Fears:

With 35.9% of those surveyed saying ‘loved ones falling seriously ill’ was what they were afraid of, and ‘economic/financial collapse’ at 37.5%, ‘loved ones dying’ at 38.1%, and becoming ‘a victim of terrorism’ at 38.5%, ‘corruption of government officials’ managed to exceed all those fears (by leaps and bounds) by coming in at a resounding 60.6%.

So, how about we demand the following Oath of Office of all our candidates for Congress, and expect the same of all our sitting members of Congress as well.

I hereby affirm that:

Since the Glass-Steagall Act of 1933 was just 37 pages long and was, at that length, long enough to prevent a severe banking crisis from happening for 75 years, I will vote against any bill that’s longer than 37 pages.

Since bills start out at X pages long when signed into law, and then become 5X pages long (full of holes and loopholes) and sometimes end up at 20X pages long (hollowed by craters a mile wide), I will vote against any legislation that is not a finished product.

I will also vote against any bill made unnecessarily convoluted, meaning: it contains stuff unrelated to what the bill was titled. I will vote against any bill made overly complicated, meaning: it contains legalese I cannot wrap my head or any head around. I will vote against any bill made into an extending labyrinth, meaning: it cross-references other bills to such an extent that the cross-referencing gets gut-wrenching.

I will reject any bill that attaches matters of secrecy or national security to material the public has a right to see. The People have a right to know what laws we lawmakers impose on them.

I will either personally read each bill I vote Yea on, or be advised by trusted advisers of every material component in each bill I vote Yea for, because I will not vote Yea unless I can submit that my knowledge of what’s in the bill is comprehensive and complete. I will communicate the logic for my yea or nay vote with my electorate, and communicate likewise with voters-at-large when the bill is of national scope and scale.

A Party “Whip” may order that all who vote for a bill, vote the Party line. Order all you want, I’ll reply, for I will vote my conscience every time, and never shy away from casting a vote that goes against the Party line. I will remind the Speaker, the Majority Leader, or anyone else acting as enforcer, that my allegiance to the People not just exceeds but supersedes my loyalty to Party.

I will vote against any bill that raises members of Congress above the laws enforced upon ordinary citizens, including those pesky insider trading rules that lawmakers always seem to find a way around.

Absent divestiture by the invested beneficiaries, I will vote against any legislation that benefits businesses in which legislators, their relatives, their associates, or their donors, are invested.

I will demand annual full disclosure of gains to income and net worth of members of Congress, and also demand that those gains be quantified exactly, meaning: I will reject any representation made in broad dollar terms, such as $1 million-to-$5 million, because there is no need for mile-wide, range-bound disclosures, unless there’s something to hide.

I will report to the Justice Department anything that smells of graft and wrongdoing. I will make records of abuse of privilege and authority, patronage, cronyism, nepotism, and any wrongful or harmful acts of favoritism, and maintain those records in safeguard. If I am harassed for them, I will make public those records.

All of the aforementioned, I affirm, because “what happens in Vegas, might stay in Vegas” but “what happens on Capitol Hill, should NOT stay on Capitol Hill.” In Vegas, people do what they do with their own money — on the Hill, they do what they do with ours.

Before we get more into the meat and potatoes of Main Street Gov’s anti-corruption drive, let’s make mention of an outlaw from English folklore, to set the pace…

From Sherwood Forest, Robin Hood took from the corrupted rich to give to the discarded poor and became a folk hero for it. From the Land of the Free and the Home of the Brave, however, our so-called public servants have instead figured a way to take from the working ordinary, and the vast majority, to give to themselves and a master amalgam of plutocrats in the minority.

So here’s to looking at Robbing The Hood by our nation’s capital, where the entrenched philosophy has become: Leave the multi-trillion-dollar causal agents of the financial crisis alone, let bankers and their most destructive instruments be, keep every handout that Wall Street or K Street gets intact, and find ways to tap-out Main Street instead, to “spread the wealth around” — the way Barack told Joe the Plumber in 2008 — except, spread it upward, to Wall Street, K Street, and their minions in Washington DC.

Want a real good example of how screwed-up everything is with those minions? Here’s how our Main Street Gov congressional candidates will be saying how…

“So you may ask why do the Wall Street wings of the Republican Party and the Democratic Party want to dismantle the Dodd-Frank Act when it’s already a nothing-burger. Because it isn’t entirely nothing. It’s got a few serious inconveniences in it, that Wall Street would rather do away with. Mostly, those serious inconveniences are related to derivatives, and to a large part those derivatives are related to a specific kind of credit derivative called a Swap.

“Whether you’ve heard of Credit Default Swaps or not, all of you will feel (or will have felt) their destructive power in late 2019, no matter what profession or industry or state of retirement you’re in.

“In 10 seconds, here’s what a Credit Default Swap is: If you’re a bank and you lend money to another bank, and you want to insure you get your money back even if the other bank goes belly-up, you buy an insurance policy from an insurer — that insurance policy then becomes the Swap.

“By 2011, America’s biggest banks had written insurance policies on as much as 50% of the total debt outstanding in the Eurozone’s most debt-ridden economies. In other words, they were on the hook for that debt, totaling Trillions of dollars. But, back then, they didn’t worry about it too much, figuring the Eurozone’s most indebted nations would work their way out of debt. Besides, there were mega-dollar premiums to collect selling those trillions in Swaps.

“On March 6 2013, with the Eurozone’s debtor nations deeper in debt, and sinking further into debt with no end in sight, those who’d sold the Swaps began to sweat. And so, with Wall and K Street pulling the strings from behind the scenes, a bill labeled H.R. 992, entitled the Swaps Regulatory Improvement Act, got introduced in the House.

“Among the sponsors of the bill: Rep. Spencer Bachus, the Republican banking committee chief who convinced then Treasury Secretary Henry Paulson (from Goldman Sachs) to do TARP bailouts in 2008, and Rep. Jim Himes — a Goldman alumnus himself, and a leader in the House alongside Chuck Schumer in the Senate overseeing the Wall Street Wing of the Democratic Party.

“Basically, H.R. 992 authorized federal assistance (translation: taxpayer bailout) to any Wall Street megabank, be it domestic or foreign, so long as it limited its swap activities to hedging or risk management (translation: if the bankers tell you it’s hedging or risk management, even if it’s not, and independent structured credit analysts say its not, it would still be covered by the taxpayer because the bankers say it is).

“On October 30th 2013, H.R. 992 sailed through the House with 292 Aye votes to 122 Nay’s. Among the Aye votes: the Wall Street Wing of the Democratic Party. (The fact that most of the Democrats from the “Banking Empire State” of New York voted Yea, ought to tell you something.) Also voting Yea was of course the usual suspects in the Wall Street Wing of the Republican Party — Eric Cantor, Paul Ryan, etcetera — and all the others who were making it up the GOP hierarchy by towing the Party line, including my opponent.

“Among the Nay votes: Rep. Walter Jones, one of four House Republicans removed from their committee assignments by Speaker John Boehner and Majority Leader Eric Cantor for defying party leadership; Rep. Tom Massie, a firebrand constitutional conservative; and Rep. Jimmy Duncan, rated the best Rep out of 435 Reps by the National Taxpayer’s Union the year before, and one of the few consistent anti-bailout stalwarts remaining in the House.

“Conspicuously skipping the vote was Nancy Pelosi who went M.I.A. And, also missing in action, was John Boehner who declined to vote as Speaker, to conveniently end up omitted from the roll call.

“In the Senate, fortunately, H.R. 992 died. Why it died there did not require rocket science — the bill was toxic to the taxpayer. Moreover, the title of the bill (the Swaps Improvement Act) advertised its toxicity for all to see, for everyone knew the “improvement” would be heading Wall Street’s way and not the taxpayer’s way.

“Fast-forward to Dec 11 2014, and you find an innocent-looking bill passing the House, with Bachus, Himes, and my opponent voting Aye for it. On Dec 13, the bill gets through the Senate. And, on Dec 16, it gets Obama’s signature to become Public Law 113-235.

“Why did this bill, that became law, look innocent at first glance? Because it was a government spending bill to keep things like salaries to our soldiers flowing, to keep the National Mall running. But that’s only if you peered at it superficially. On closer inspection however, on page 250 of the bill, lo-and-behold what do you find: the authorization for bailouts of failing Swaps — in aggregate total, trillions of dollars of Swaps.

“Now they’ll argue the contracts for these swaps might total Trillions of dollars in so-called notional value, but if you were to net them out, they’d net out to little or nothing. But then why hide them in a government spending bill? Why do this just days away from the Christmas holidays? Why let Citigroup ghostwrite that page of the bill? Why were Wall Street execs gunning for passage of the bill? Why was a Chairman and CEO of a megabank working the phones to line up votes for passage of the bill?

“Answer is: because their “net out to little or nothing” argument was baloney. Sure, Swaps can net out normally when there’s no systemwide meltdown. But when banks begin to collapse in tandem, like dominos, like they did in Sep 2008, the net ain’t little or nothing — far from it. In a systemic banking crisis, of the kind a fracture in the Eurozone can trigger, the net can explode towards notional, fast!

“The hiding of bailouts and handouts to bankers in a government spending bill is no surprise really. In 2009, having bailed out A.I.G. to the tune of $182 Billion, Congress hid a $450 million bundle of bonuses to the bankers who bankrupted A.I.G. in an Economic Stimulus Bill. So this too was true to pattern. Except, when I get to Congress, I’ll put an end to that pattern, pronto.”

As we documented under our Crisis bill about the Eurozone:

The euro, as we now know it, will not survive. Why? For myriad and manifold reasons, from the social all the way out to the fiscal, such as the anti-Muslim-migrant alliance developing between political parties in Italy, Spain, Portugal, Greece, Ireland, Austria, the Czech Republic, Hungary, Poland, Slovakia, and Slovenia, to (among other matters of German self-interest, AND SELF-PRESERVATION) the trajectory of Berlin’s Target-2 balances.

The former is to be expected. The ultra-conservative European media is incessant in its coverage of migrant crime, and, as a result, nationalist right-wing parties are on the rise in the aforementioned countries of Europe.

But the latter is less well known and, consequently, less anticipated. In essence, the German Target-2 tangent is the epitome of unsustainable. The math alone will tell you why… By early 2017, Germany’s Target-2 claims (for simplicity, think of it as money owed to Germany by Italy, Spain, and other effectively bankrupt debtor nations) was fast approaching one-third of German GDP. In Feb 2017 alone, it rose by €20 billion. On the flip side: in March 2017, Spain’s Target-2 liabilities surged to a record €374 billion; in March 2017, Italy’s Target-2 liabilities surged to a record €419 billion.

Across the board, across the Eurozone, these numerals, from both the debtor and creditor perspectives, are deteriorating, not ameliorating, at least not consistently — consider: in 2006, German claims totaled just €5 billion; in 2016, that number rocketed past €700 billion; July 31 2017, per the Deutsche Bundesbank, it’d surpassed €856 billion. It’s political suicide for any politician, be they in the Reich Chancellery or the Deutscher Bundestag, to allow such a tangent for too long.

It’s already been too long for the Bundesbank, which is why we hear, through a grapevine we consider reliable, that agents of the Germany’s central bank have drawn up ‘exigent’ ‘contingency’ ‘protocols’ for a sudden and unannounced German exit from the euro and a concurrent German re-entry into the Deutsche Mark, over a long weekend that extends a banking holiday ‘at least 2 days into the workweek’ in a government-mandated ban on cross-border transactional activity.

Thus, as we see it, in 2019 (perhaps toward the latter part of the year) Germany will exit the Euro and revert to the Deutsche Mark. Creditor nations, like Finland, will follow Germany’s lead and leave the Eurozone as well. For a while thereafter, until 2021 or thereabouts, the Euro will be retained by Latin Europe and other debtor nations in what remains of the Eurozone. France may lead that remnant of a monetary union for a while, until it too realizes its own amassing exposure to foreign debt, and quit, the way Germany did. In 2021 or thereabouts, the Eurozone’s status as an economic power-bloc will finally come to an end. Whether a severely devalued currency still called a euro survives past 2021 in Greece, Portugal, Spain, Italy, Ireland, or elsewhere, remains to be seen.

So, when the Eurozone fractures and then disintegrates, those Swaps (that our congressional candidates reference) will deliver one helluva thumping to whoever’s left holding them. Which is why the biggie-banks did what they did, to unload them.

So, yes, as usual into the thick of the holidays, when public attention to such matters runs light and lenient with Christmas and New Year around the corner , the megabanks got the Congress and the White House to wrap some $7 Trillion in flammable derivatives around the neck of the taxpayer, by having the provision inserted into a must-pass government appropriations bill. (And, no, the fat-cats didn’t write the taxpayer a check for all the premiums earned selling those Swaps. Those, they kept in their belly-lining bonuses.)

And, yes, the Congressional Budget Office did go so far as to prognosticate that the $7 Trillion or so in Swaps was, technically-speaking, an aggregate ‘notional’ number and not a counterbalanced ‘net’ number, despite knowing full-well that ‘notional’ can fast converge upon ‘net’ when financial counterparties fall in tandem, in a cascading domino effect, that turns what would normally be an orderly bank-by-bank failure into a systemwide banking collapse en masse — ask Joseph Cassano, the ex-head of A.I.G. Financial Products, if you have any doubt about that. (Actually, we’ll ask him for you at the bottom of this page.)

For the record:

The effort was led by the debt & deficit “hawks” in the Democratic Party and co-led by the debt & deficit “hawks” in the Republican Party.

“I think [the bill] reflects the people’s priorities,” gushed Speaker John Boehner, without shedding a tear for what a whopper that was. Normally, he’d cry up a river for much less, you might recall.

Anyway, within days President Barack Obama , who also personally lobbied for passage of the bill, signed the atrocity.

That, ladies and gentlemen, is just one example of how they stick it to us, up there in Washington DC.

And, so, the urgent need for a template to rightfully restore in our Presidents, Secretaries, Members of Congress, and all their appointed officials and staff, the Jeffersonian code of “retiring with hands clean, as they are empty” and to telling any Teflon Don’s and Donatella’s in Washington DC — who might be feeling invincible — that it’s GREASE they’re covered in, NOT TEFLON!

Now, for two takes on corruption at play. The first relates to Big Pharma. The second pertains to polar bears … yes, those fuzzy Arctic furballs that Goldman Sachs says it cares so much about.

Take 1:

In 2016, Big Pharma spent more than $150 million lobbying Congress to oppose any reform that would take away from the bottom line profit that was feeding their billions of dollars in executive compensation, including any reform to allow for the importation of pharmaceutical drugs from high-safety-standard countries like Canada. For your information, in 2015 the profits of the 20 biggest pharmaceutical corporations totaled $125 Billion

So that you know…

Health Canada, Canada’s equivalent to America’s Food & Drug Administration, maintains safety standards on par with our FDA.

Online Canadian pharmacies, licensed by local authorities, bear accreditation from the Canadian International Pharmacy Association.

Medicines received from licensed Canadian pharmacies, bearing Canadian International Pharmacy Association accreditation, have the Health Canada stamp of approval on them.

Now, we all know that most Republicans protect big business interests no matter how steep the cost inflicted upon Main Street gets. But many Democrats are not much better.

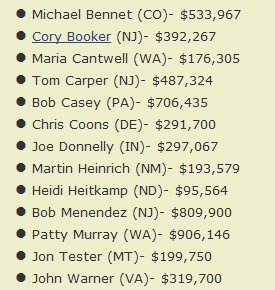

On Jan 11 2017 Senator Amy Klobuchar [D-MN] sponsored (and Senator Bernie Sanders co-sponsored) an amendment to allow for the importation of pharmaceutical drugs from countries like Canada. Twelve Republicans voted in favor of that amendment. But then the cost-savings measure — to cut drug prices down dramatically for the benefit of American patients and consumers, and taxpayers overall — got killed by 13 Democrats who voted against it.

Who those Democrats are and how many dollars they’ve taken in from corporate pharmaceutical giants can be found HERE.

In general, the 13 Democrats cited safety standards for their rejection of the amendment. None of them made any mention of the $$$-contributions they’d taken in from their Big Pharma donors, at least not publicly.

Take 2:

Before we get into the polar bear part, right from the get-go let us make a stance of ours clear, in advance. Main Street Gov’s team — which counts conservatives, libertarians, independents and centrists to its composition — supports the U.S. fossil fuel industry for the jobs they provide and the choice they enable in how we choose to mechanize. Yet, we despise a number of nation states who’ve made fossil fuels their weapon of choice to aggress, suppress, and deny — and by that we mean: fossil fuel dependence by man has spawned and financed the continuance and endurance of a number of undesirables throughout the world, from autocratic and despotic monarchies that have zero tolerance for fundamental human rights, to terrorists who shed the blood of innocents with recruits and armaments procured with money generated off black market sales of fossil fuel. We believe fusion technology will, in a little over a decade or so, replace man’s dependence on fossil fuels, anyway. And, when that someday comes, it will save all of us consumers a lot of expense, as fusion tech is energy on the cheap, like you can’t imagine. Jobs lost to the sea-change, will be regained.

Whether you like fossil fuels or not, nobody with any semblance of a sensory system likes pollution, of course … except that is for bankers. Too Big To Fail bankers have long eyed an opportunity to monetize fossil fuel pollution to fatten their behinds — they just haven’t had a chance to harvest that fat, yet. Matt Taibbi explored the intersection between ‘mega-banking’ and so-called ‘man-made global warming’ quite a bit in the Rolling Stone article: The Great American Bubble Machine — [how] Goldman Sachs has engineered every major market manipulation since the Great Depression, and [how] they’re about to do it again (scroll down to: “BUBBLE #6: Global Warming” if you’d like to see his input on the matter).

The exchange of cap-and-trade/carbon-credits is a place of securitization (and profit) that bankers want to take their climate change/global warming agenda to — much like they did with their ‘affordable housing’ agenda, via securitized mortgages of the subprime kind. That securitized exchange could be worth many tens of billions of dollars of revenue to Wall Street, annually. As for Wall Street insistence that it also cares about polar bears having enough ice to perch on… look, when we hear any of Goldman’s executives (especially) voicing concern for the environment, it always gets us laughing, like the time Goldman CEO Lloyd Blankfein did HERE. Why, because while you and I embrace the idea of keeping our planet clean and pristine for unselfish reasons, there are also those who’ve made “clean and pristine” an agenda for purely selfish ones.

Again, the business of ‘cap-and-trade/carbon-credits’ could be worth gazillions to Wall Street if the megabanks have their way, and megabankers have purchased just about everybody they can, to someday have their way. You’ll have an inkling of who’s bought-and-paid-for by a simple measure: by whether they practice what they preach, to protect the environment that they say they hold so dear.

Needless to say, when bankers, their surrogates, and their proxies say they care about the welfare of your great-grandkids, or the well-being of polar bears, the marine life they eco-depend on and the fish they feed on, you know something’s fishy.

The meltdown in Japan’s Fukushima nuclear reactor, that began March 2011, is (as of this writing) an ongoing hyper-contaminant of our Pacific Ocean at the rate of 200+ tons per day, with 300 tons of contamination per day reported ‘officially’ in late 2013, per Reuters. Yet, neither banker nor proxy talks about it. Perhaps because there’s no money to be made in it, that they can think of.

After the Tokyo Electric Power Company’s chairman, Takashi Kawamura, suggested dumping 777,000 tons of radioactive Fukushima water into the Pacific Ocean, President Barack Obama, Establishment environmentalists, and the Mainstream Media remained eerily silent. Normally, they’d raise a storm over any bombardment of the environment.

(FYI: 5 of 6 Fukushima plants were General Electric Mark 1 reactors; 35 years ago, their design was found to be defective by GE’s own evaluators, who resigned in protest, after their evaluation got shelved; GE’s CEO has figured prominently inside both the Obama & Trump Administrations.)

In Oct 2015, Eco-Business reported that carbon emissions from Indonesia’s peat fires — greenhouse gases from peat fires in Borneo and Sumatra, specifically — exceed those of the entire US economy. We don’t see that from any of the talking heads in the Establishment or the mainstream media.

Carbon dioxide is a greenhouse gas. It is the primary emission blamed for climate change by bankers and their spox’s. Yet, at the heart of the continental United States is our very own super-CO2-spewing super-volcanic Yellowstone National Park — a 2008 field campaign highlighted by the United States Geological Survey, a government agency, found that Yellowstone’s Brimstone Basin released 277 metric tons of carbon dioxide from the ground PER DAY.

China has long promised to cap and reduce carbon emissions, but done the 180-degree polar opposite. The New York Times would in Nov 2015 detail how 155 coal power plants got approval for construction in China in just the first 9 months of 2015, equating to 40% of the operational capacity of all the coal power plants in the entire United States.

China’s Shenhua Group says it expects to produce 278 million tonnes of coal in 2017. (1 tonne=1 metric ton=1000 kilograms.) In 2016, Shenhua produced only 8% of China’s total coal output.

In 2016, U.S. coal production totaled 728 million short tons. (1 short ton=2,000 pounds, compared to 1 metric ton, or tonne, being equal to 2,205 pounds.) In 2016, China’s coal production totaled 3,210 million metric tons, or 3,539 short tons — almost 5 times that of the U.S.

Just one of China’s many big coal producing companies, Shenhua Group, employed almost 200,000 coal miners — that’s more than 2.5 times the number of coal miners you’ll find in the entire U.S. coal mining industry.

Eleven other countries (other than America, that is) produced 6,692 million short tons of coal in 2016 — about 9.2 times U.S. output that year.

That the biggest polluters on earth, like China under communist rule, might diplomatically nod to, but never agree to (much less abide by) cap-and-trade and the exchange of carbon credits, goes largely unmentioned.

That Chinese government officials routinely dismisses global warming as a “pseudo science” is lost in translation.

That Russian government officials routinely dismisses global warming as a “bogus science” is lost in translation, as well.

No problem of any kind, affecting the Earth as a whole, can ever be solved by a few dozen countries if the other ‘196 countries minus those few dozen’ dismiss it, or outright laugh it off. Of course, the bankers at Goldman Sachs know that — but there’s gobs of money to be made in even the few dozen countries going it alone, so they’re going for it anyway. Their emissaries, some of whom posed for this most regal photo at the Paris climate summit of Nov 2015, are not just their mouthpieces, but also their marionettes.

There are 4 mission-critical add-on elements to our anti-corruption drive:

Element 1

In a banana republic, a politician is handed a briefcase of cash in exchange for political access and favor. In America, the problem with the briefcase idea is, more often than not, a briefcase would not be big enough. Often enough, even a suitcase would not be big enough. Given enough exchanges over time, the kind of truck-sized container you see aboard a cargo ship would not be big enough.

Take for example our former Secretaries of the Treasury and State, who used to earn less than $200,000 in office in a whole year, now raking in more than $200,000 in less than an hour.

Take for example a former Chairman of the Federal Reserve, who used to earn a wee bit less than $200,000 in a year, charging hedge fund honchos a wee bit more, just to have one single sitdown dinner with him.

Take for example the $400,000 and the $3.2 million for two brief speaking engagements, pulled in (in the bat of an eyelid) by the latest ex-president of ours.

Also, take for example a former president of ours, paid $700,000 to speak in Lagos Nigeria, a dollar amount that corresponds to about 240 times what the average citizen of Nigeria earns in a whole year. At the time of the speech, Nigeria had 100 million of its people (out of 160 million in total) living in abject poverty. (By the way, that $700K got paid twice in two years to the ex-president in question.)

So, in light of all this public $ervice dollars sloshing around, how about we mandate that all proceeds from book deals, speaking appearances, sitdown dinners, or any other comparable activity, be it here or abroad, be donated to a worthy charity — and, by “a worthy charity” we mean one that gives near-all its money to those in need, and not to those who claim to work for those in need.

So, yes, that $1.5 million a former President of ours got for a Q&A session with Swiss banking behemoth, UBS, while UBS was under investigation by the IRS for enabling tax evasion — a probe that ended up largely dropped, in what could’ve been quid pro quo — should’ve gone to a worthy charity.

Element 2

Elsewhere on this website, we spoke about the possibility of “payoffs” to ex government officials “making their way to bearer bonds in numbered accounts, inside bastions of banking across the pond.” With respect to that, let it be made clear that any banker, in Europe or anywhere else, found aiding and abetting the concealment of funds by current or former U.S. Government officials, risks two plights:

- At the personal level, risk of indictment in the year 2021 by a U.S. Justice Department of a kind and character never before seen.

- At the institutional level, risk to the function and continuity of his or her employer’s banking operations that fall under U.S. jurisdiction

Want to do business in the U.S. dollar in the year 2021 and beyond? Then tell us who these unlawful miscreants are, or we will deny you a license to transact in the U.S. dollar — such a denial, Mr. Banker, you know is a death sentence for your bank, no matter where you are.

Element 3

How about paying the salaries of the President, Members of Congress, the Secretary of the Treasury, and the Chair of the Federal Reserve, in some combination of cash and Long Term Treasury Bonds, instead of all cash, so that they aren’t so quick to do bailouts, for anyone!

The last financial crisis catapulted the tangent of the nation’s debt onto a highly elevated trajectory, and the next could send it up disconcertingly close to a right angle, so how about we put the payroll of our politicians, and the salaries of our alleged Guardians of the People’s Money, at the mercy of Bond Vigilantes?

Element 4

To seal all revolving doors shut, how about we make it law of the land that one cannot work in government and work in industries regulated by government — EVER — beginning with (a) banking, finance, insurance, and real estate (b) pharmaceuticals and healthcare, and (c) energy, oil and gas.

Moreover, as part of the effort to permanently shut down Capitol Hill cross-traffic through the revolving door, let us support a return of Congressional staff onto an effective federal pensions plan if they leave Congress after many years of dutiful service.

Basically, in order to keep the purveyors of our nation’s legislation off both Wall Street and K Street, we need to show them the way to Main Street.

Honorary Mention

There are bad apples in every basket. Usually, they are at the bottom. On Wall Street, however, they are often at the top. The aforementioned Joseph Cassano, former head of AIG’s Financial Products division, or AIGFP, is highly representative of that configuration.

Running AIGFP and talking General Relativity first, the young Einstein first told AIG’s general management how they’d relate to each other, as in, quote: “You know insurance, I know investments, so you do what you do, and I’ll do what I do.”

That understanding next allowed him the leeway to take in as much as one-half Trillion dollars in bets—mostly in the form of Credit Default Swaps — without a worry in the world as to how he’d cover them, in case those bets (Swaps) went against him.

By August 2007, with housing in collapse, and his bets tethered to that collapse by a noose, Cassano moved calmly onto the Theory of Special Relativity, theorizing, quote: “It is hard for us … to even see a scenario … [of] us losing one dollar, in any of those transactions.”

If he meant $1 only — and not specifically many tens of billions of dollars, or $62 billion in just one 90-day span — then, in all fairness to the guy, his Special Theory remains intact. But, of course, that’s not what the numbskull meant.

Forced to resign by March 2008 for setting fire to AIG, Cassano was punished, like every other arsonist, with $1 million a month in consulting fees (part-paid by the government), and a nostalgic reminder by AIG’s government-appointed CEO, Martin Sullivan, to Congress, that “the 20-year knowledge that Mr. Cassano had” was priceless.

Yes, lose enough money to require a $182 billion taxpayer bailout, and you’re suddenly a genius in Washington DC!

But you know what? In hindsight, maybe what Cassano knew was priceless. And maybe he was a genius after all. Perhaps we just failed to appreciate it. For here’s a guy who near single-handedly set a nerve-numbing world-record for the most money lost by an American institution in the shortest amount of time, after placing tons-upon-tons in bets he knew he could not honor if those bets went against him, and yet — yet! — he got the United States Government to hand him and his company a rescue that was TWICE THE SIZE of Russia’s defense budget.

And, despite having done all that — on top of it all — he still got to walk away from all the carnage he wreaked, scot-free, with both his hide and his $315 million loot intact, with a bonus added-on.

That is priceless, that is genius, come to think of it.

It’s been widely reported that Cassano liked to tell his employees: “When you lose money, it’s my f**king money.”

After everything that happened, we’re sure he’s tweaked that a bit to say: “When I lose money, it’s YOUR f**king money.”

To know that the US Government would 100% abide by his ‘my money, your money’ theorem — also known as the ‘heads I win, tails you lose’ rule — took real smarts, we have to admit.

Living it up in England now, Cassano might tell you that, too, if he could. This photo of him peeking from behind a wall at his lavish townhouse near the world-famous Harrod’s of London, may even be Joey telling you that.

With all of the aforementioned mini-bio of Joey in mind, now realize:

In Sep 2008, with the blessings of Timothy Geithner at the New York Fed and others above and below him, AIGFP would serve as Trojan Horse for the plunder of the US taxpayer, by banks both domestic and foreign.

Within 6 months of that pillage, the derivatives traders of AIGFP would listen to unbelievable music playing in their disbelieving ears — a mix of acid rock, rave, gangsta rap, and swing — of $450 million in bonuses being paid to them, despite all they’d done wrong, on the statutory authority of no less than the Government of the United States.

And where was that statutory authority to pay $450 million in bonuses planted? In the “The American Recovery and Reinvestment Act” or “Stimulus” Bill.

Enacted by the 111th Congress and signed by the President on Feb 17 2009, the Bill’s $450 million included $34 million gift-wrapped and ribbon-tied to Cassano himself.

And we couldn’t help but imagine Joey Cassano thinking:

Who else would pay bonuses to the bankrupters of a company, than a Government-owned company?

And who else would hide those bonuses in an economic Stimulus Bill, than a Government as messed-up as this!

You’ve just read in full our Reasoning & Rationale for this Bill-Request. We sincerely hope we’ve given you enough to vote in support of it.

{kind=link}

{kind=link}

{kind=link}

{kind=link}